Meta Description: After Fed rate cuts, 30-year mortgage rates are expected to fall toward ~5.9% by end of 2026. Learn how these cuts affect home buyers, the housing market, bonds, and your refinancing strategy — explained in full detail.

Focus Keyword: Fed rate cuts mortgage rates 2026

Introduction: Is Now the Right Time to Buy a Home?

If you have been dreaming of buying a home for the past few years but held back because of high mortgage rates, 2026 could finally be your window. Following a series of Federal Reserve (Fed) rate cuts, analysts widely expect 30-year fixed mortgage rates to trend downward — with some forecasts projecting rates as low as 5.5% to 5.9% by the end of 2026.

But the picture is not straightforward. The relationship between Fed rate decisions and mortgage rates is more complex than most people realize. In this article, we break down everything you need to know: where rates are headed, why, and what it means for home buyers, homeowners, investors, and anyone watching the housing market.

What Are Fed Rate Cuts?

The Federal Reserve is America’s central bank. It controls the federal funds rate — the interest rate at which banks lend money to each other overnight. When the Fed lowers this rate, borrowing becomes cheaper across the entire economy: for businesses, consumers, and banks alike.

The Fed cut rates three times in 2024, and continued with additional cuts in the second half of 2025. Heading into 2026, markets are pricing in two to three more cuts — which, in theory, should push mortgage rates lower.

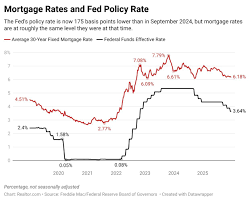

However — and this is a crucial point — 30-year fixed mortgage rates do not move in direct lockstep with the federal funds rate.

How Are Mortgage Rates Actually Determined?

This surprises many people. The 30-year fixed mortgage rate tracks the 10-year U.S. Treasury bond yield far more closely than the Fed funds rate. When investors are confident in the economy, they sell bonds (yields rise, rates go up). When uncertainty grows, they buy bonds (yields fall, rates go down).

Beyond Treasury yields, mortgage rates are shaped by:

- Inflation: Higher inflation keeps rates elevated. The Fed’s target is 2% CPI.

- Economic growth: Recession fears push rates down as investors flee to bonds.

- Geopolitical events: The Iran conflict in early 2026 temporarily pushed oil prices — and mortgage rates — back up toward 6.5%.

- Investor demand: Demand for mortgage-backed securities influences rate spreads.

- Fed policy signals: Forward guidance matters as much as actual cuts.

Historical data shows: for every 1% the Fed cuts, mortgage rates typically fall only 0.6% to 0.8% — not one-for-one.

2026 Mortgage Rate Forecasts: What the Experts Are Saying

Major financial institutions and housing analysts have published their forecasts for where 30-year fixed mortgage rates are headed in 2026. Here is a summary:

| Institution | 2026 Forecast (30-Year Fixed) |

|---|---|

| Fannie Mae | ~6.0% |

| Redfin | ~6.3% |

| Realtor.com | ~6.3% |

| Zillow | Above 6.0% |

| Bankrate (Ted Rossman) | 5.5% – 6.5% (range) |

| TD Bank Economic Group | ~6.14% average |

| Mortgage-Info.com | 5.50% – 6.00% (year-end) |

Most forecasts cluster around the 6.0% – 6.3% range for the majority of 2026. However, a few optimistic analysts — including Bankrate’s Ted Rossman — believe rates could dip below 6% for the first time since summer 2022, potentially reaching 5.5% to 5.9% under favorable conditions.

The 5.9% Target: Realistic or Just Optimism?

So can 30-year mortgage rates actually reach ~5.9% by the end of 2026? The answer is: yes, but only under a specific set of conditions.

Condition 1: The Fed must deliver 2–3 rate cuts

Markets currently expect the Fed to cut rates two to three times in 2026. If a larger “jumbo cut” of 0.50% arrives — particularly in the June–September window — it would signal economic softness and likely pull mortgage rates meaningfully lower.

Condition 2: Inflation must cool toward 2%

The Fed’s inflation target is 2%. If the Consumer Price Index (CPI) approaches this level, the Fed gains the room to cut rates more aggressively. Geopolitical tensions in early 2026 pushed oil prices higher, temporarily complicating the inflation picture.

Condition 3: Treasury yields must fall below 4%

The 10-year Treasury yield currently sits in the 4.3% – 4.6% range. For mortgage rates to drop to 5.9%, this yield would likely need to fall below 4.0% — which typically happens when economic growth slows or recession fears mount.

Condition 4: No new geopolitical shocks

The Iran conflict in early 2026 was a reminder that external shocks can derail rate forecasts quickly. Absent such disruptions, the gradual downward trend in rates is expected to continue.

Bottom line: 5.9% is achievable, but far from guaranteed. The most realistic expectation for year-end 2026 is a 30-year rate in the 5.75% – 6.25% range, depending on how economic conditions evolve.

Where Are Mortgage Rates Right Now?

As of June 2026, 30-year fixed mortgage rates are sitting in the 6.4% – 6.5% range — slightly elevated compared to late 2025 due to geopolitical-driven inflation concerns. This is well below the 2023 peak of approximately 7.79%, but still historically high enough to keep many buyers on the sidelines.

The good news: the broader trend since late 2023 has been downward, and most analysts expect this to continue through the rest of 2026.

Impact on the Housing Market

Mortgage rates do not just affect monthly payments — they reshape the entire housing market in ways that ripple out for years.

The “lock-in effect” begins to unwind

Millions of homeowners locked in mortgage rates of 2% – 3% during the pandemic. They have been reluctant to sell because doing so would mean taking on a new mortgage at 6%+. As rates gradually fall toward 5.5% – 6%, more of these homeowners will be willing to move — unlocking supply that the market desperately needs.

First-time buyers get meaningful relief

Lower rates directly increase purchasing power. Here is what the math looks like on a $400,000 home purchase:

- At 7.0%: monthly payment ≈ $2,661

- At 5.9%: monthly payment ≈ $2,375

- Difference: $286/month — $3,432/year

For a family budgeting carefully, that is a significant difference in what they can afford.

Home prices may rise again

Lower rates tend to stimulate demand. If more buyers enter the market before inventory catches up, prices could accelerate — partially offsetting the affordability gains from lower rates. Bright MLS chief economist Lisa Sturtevant notes that “slightly lower rates and slower price growth should improve affordability a little, which could bring more buyers into the market” — but it is not a complete solution.

What This Means for Bonds and Investors

Falling rates do not just affect home buyers — they reshape returns across financial markets.

Bond investors benefit

When the Fed cuts rates, existing bonds that pay higher yields become more valuable. If you hold a 10-year Treasury at 4.5% today and the Fed cuts by 1.25%, newly issued bonds will pay only around 3.8% — making your bond worth 5% to 8% more in the secondary market.

Savings accounts will pay less

This is the flip side that many people overlook. As the Fed cuts, high-yield savings account rates will fall proportionally:

- Current high-yield savings: ~4.5% APY

- After 2–3 Fed cuts: ~3.0% – 3.5% APY

On a $50,000 balance, that translates to earning $500 – $750 less per year. Strategy: lock in 1–2 year CDs now at 4.8% – 5.0% before rates fall.

Should You Buy a Home Now or Wait?

This is the most consequential question for millions of Americans. The honest answer: it depends on your personal financial situation — not just on rates.

Reasons to buy now:

- Less buyer competition means fewer bidding wars

- Sellers are more willing to negotiate on price and concessions

- If rates drop, you can refinance later (“date the rate, marry the house”)

- Home prices continue to appreciate — waiting may mean paying more

Reasons to wait:

- A 5.9% rate instead of 6.5% saves ~$150/month on a $300,000 mortgage

- More inventory may become available as the lock-in effect unwinds

- Waiting gives more time to build a larger down payment

General rule: If you plan to stay in the home for 7 or more years, buying today at a higher rate can still make financial sense — especially with refinancing options available. If your timeline is shorter, waiting for rate relief may be wiser.

Refinancing Strategy: When and How to Act

For existing homeowners, 2026 presents a potential refinancing opportunity — but only if the math works out.

The break-even rule

Refinancing typically costs $3,000 – $5,000 in closing costs. The standard guidance: only refinance when you can reduce your rate by at least 0.75% – 1.0%. That creates enough monthly savings to recover the upfront cost within a reasonable timeframe.

Example: Refinancing a $300,000 mortgage from 7.0% to 6.0% saves roughly $200/month. With $4,000 in closing costs, you break even in 20 months — a solid deal if you plan to stay put.

Best refinancing window in 2026

Most analysts expect the most significant rate drops in the June – September 2026 period, when a larger Fed cut is possible. Set rate alerts with your lender, and be prepared to lock in a rate 45–60 days before closing to protect yourself against sudden upward moves.

Three Scenarios for Year-End 2026

Given all the variables involved, here is a realistic range of outcomes:

| Scenario | Conditions | 30-Year Rate |

|---|---|---|

| Optimistic | 3+ Fed cuts, inflation at 2%, no shocks | 5.5% – 5.9% |

| Base case | 2 Fed cuts, moderate inflation, slow growth | 6.0% – 6.3% |

| Pessimistic | 1 or 0 cuts, inflation rebounds | 6.5% – 7.0% |

Key Takeaways

- 30-year mortgage rates track 10-year Treasury yields, not the Fed funds rate directly — the relationship is indirect and imperfect.

- Rates of 5.9% by year-end 2026 are possible but represent an optimistic scenario; the base case is 6.0% – 6.3%.

- The housing market will benefit from lower rates, but home price increases could partially offset affordability gains.

- Savings account yields will fall as the Fed cuts — lock in CDs now if you have cash sitting idle.

- The June – September 2026 window is the most likely period for peak rate relief and refinancing opportunity.

- Whether to buy now or wait depends far more on your personal financial stability than on rate movements alone.

Conclusion: Rates Are Falling — But Patience Is Required

The direction of travel for interest rates is clear: downward. Whether 30-year mortgage rates reach the symbolic 5.9% threshold by the end of 2026 depends on a combination of Fed decisions, inflation data, geopolitical stability, and investor sentiment — all of which remain genuinely uncertain.

What is certain is that the worst of the rate spike that began in 2022 is behind us. For buyers who have been waiting on the sidelines, the opportunity window is gradually opening. For homeowners in high-rate mortgages, the refinancing opportunity of the next 12 months is worth watching closely.

The best strategy: stay informed, improve your credit score, keep saving your down payment, and be ready to move decisively when rates hit your personal target. Because when 5.9% does arrive — whether in 2026 or early 2027 — the buyers who prepared will be the ones who benefit most.